Do You Know How Car Loans Work? Understanding the Easy Auto Financing Process

Posted Friday, Jan 16, 2026

Buying a car—whether it's a new vehicle or a reliable used car—often requires financing. Understanding how the auto financing process works matters because it affects your monthly payment, total interest paid over the life of the loan, and how quickly you can repay the loan. A clear grasp of loan terms, APR, credit score impact, and financing options helps you finance a car with confidence and find a good auto loan.

How does my credit score affect my ability to get a car loan?

Your credit score is one of the most important factors lenders use when evaluating loan applications. A higher credit score typically unlocks lower interest rates and better loan offers, while a lower score can lead to higher loan rates or even a denial for an auto loan. When you apply to get a car loan, lenders check your credit history and credit report to estimate your risk and set the APR and loan term.

Example: If your credit score is strong, you may qualify for a lower loan rate and a shorter loan term that reduces the total interest over the life of the loan. Conversely, if your credit report shows late payments or a limited credit history, consider working with a credit union or other auto lenders that offer flexible financing options, or make a down payment to lower the loan amount.

What should I check on my credit report before applying?

Always review your credit report for errors, outdated information, or missed payments. Correcting inaccuracies can improve your credit history and increase your chance of being approved for a loan. Use the free annual credit report service to confirm the accounts, balances, and any factors that might affect your interest rate.

Tips: Dispute errors early, pay down revolving balances, and avoid applying for multiple loans at once—loan applications within a short window can still impact your score, though multiple auto loan inquiries are often treated as a single inquiry by scoring models.

What financing options do dealerships and lenders offer to finance a car?

Dealerships, credit unions, banks, and online auto lenders all offer financing options. Dealerships may provide convenience and on-site loan offers to get manufacturer incentives for new vehicles, while credit unions frequently offer lower loan rates and more personalized service. Comparing loan offers from multiple sources gives you leverage to find the best loan and lower interest over the life of the loan.

Common options include traditional car loans, leasing a car, and, in some cases dealer-backed financing or subprime auto loans. Each option affects your monthly car payment and total interest: leasing can mean lower monthly payments, but you don't own the vehicle at the end, while financing a new or used car lets you pay off the loan and purchase the car outright.

How can I compare loan offers effectively?

Use an auto loan calculator to estimate monthly payments for different loan terms and APRs. When comparing, look at APR and loan term together, because a lower monthly payment from a longer loan term can increase the total interest you'll pay. Compare loan rate, fees, and any dealer incentives to find the best loan for your budget.

Checklist: Compare the annual percentage rate (APR), loan amount, loan term, monthly payment, and total interest. Consider the principal and interest breakdown and whether prepayment penalties exist if you decide to pay off the loan early.

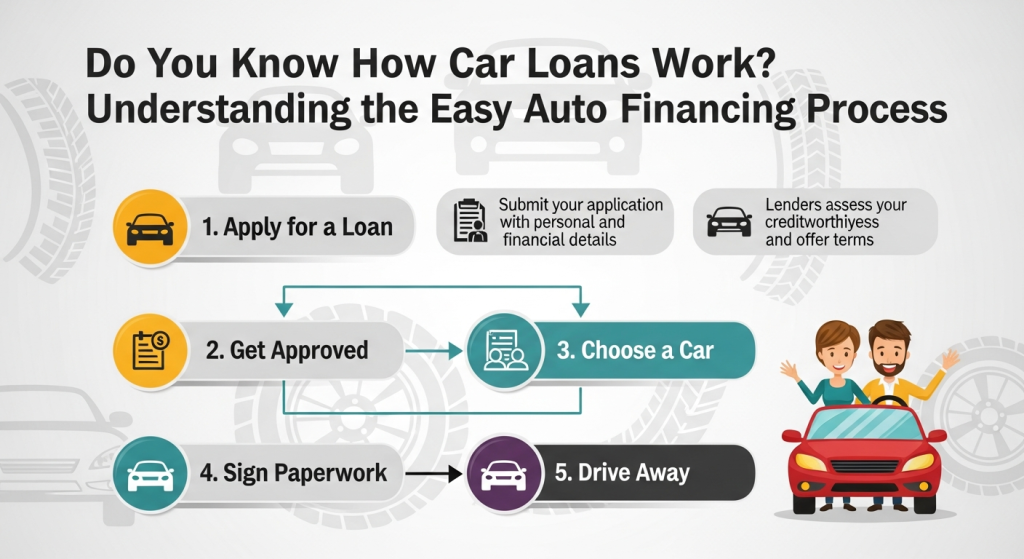

How easy is it to get approved for a loan and what are typical loan application steps?

The loan process is often straightforward: check your credit report, determine your budget, choose a vehicle, gather documents, and submit loan applications. Many lenders offer quick online approval often known as "fact approval car loan" or pre-approval that helps you negotiate confidently at the dealership. Getting pre-approved shows the loan amount you're approved for and the loan rate you can expect.

Documents typically include proof of income, ID, proof of residence, and information about the vehicle. Some buyers may also use pay stubs, bank statements, or tax returns for self-employed applicants. Pre-approval does not commit you but streamlines the purchase process and helps you understand the monthly car payment you can afford.

What does pre-approval or fact approval car loan mean?

Pre-approval (fact approval) definition:

- A lender has reviewed your credit profile and agreed in principle to lend a specific loan amount at an estimated APR and terms.

- Simplifies shopping by showing sellers that you are a serious buyer ready to purchase a car.

- Note: The final loan offer may change slightly based on the exact vehicle, down payment, and finalized documentation.

Benefits of pre-approval:

- Provides a clear budget for purchasing the car.

- Speeds up dealership paperwork.

- Gives leverage to negotiate price.

- Pre-approved loan rate may be superseded by a better dealer offer or a lower rate from another auto lender if you shop around.

How do loan term and APR affect my monthly payment and total interest?

The loan term (length of time) and APR (annual percentage rate) directly determine your monthly payment and the total interest you pay over the loan's life. Shorter loan terms usually have higher monthly payments but much lower total interest. Longer loan terms reduce monthly payments but increase the total interest, which can make the loan more expensive over time.

Example: A $20,000 loan at a 5% APR for 36 months will have a higher monthly payment than the same loan extended to 72 months, but the shorter loan will result in less total interest. Use an auto loan calculator to compare scenarios and see the life of the loan impact on total interest and principal and interest split.

Should I choose a shorter or longer loan term?

Choose a loan term based on your budget and goals. If you want to minimize total interest and possibly secure a lower loan rate, opt for a shorter loan term. If your priority is a lower monthly car payment to fit current finances, a longer loan term can help—but watch the interest over the life of the loan and the possibility of negative equity if the vehicle depreciates faster than you pay down the loan balance.

Tip: Find a balance—choose the shortest term that provides a comfortable monthly payment while avoiding excessive total interest. Consider making extra payments to pay off the loan early without extending the loan term unnecessarily.

What role does down payment play when you finance a used car or new car?

A down payment lowers the loan amount you need to finance and can reduce your loan rate if it improves your loan-to-value ratio. Making a down payment helps you avoid being upside-down (owing more than the car is worth) and can make it easier to get approved for a better auto loan, especially on used cars where depreciation has already occurred.

Practical example: A larger down payment reduces monthly car payments and can qualify you for lower APRs, particularly with lenders like credit unions that may offer better loan rates when the loan-to-value is lower. If you’re financing a used car in Winter Garden, FL, or elsewhere, a down payment can be the difference between approval and a high-interest loan.

How much should I put down to get the best loan terms?

While 20% is a common recommendation for a down payment to protect against depreciation and secure favorable loan options, even a smaller down payment can help. The ideal down payment depends on the car price, your credit score, and whether you’re buying used or new. For used cars, lenders sometimes require larger down payments to mitigate higher risk.

Strategy: If you can’t afford 20%, aim for at least enough to bring the loan-to-value below 100% and reduce the loan amount. Combine down payment with trade-in value to further lower the loan principal.

How do dealerships and credit unions differ when you finance a car?

Dealerships often offer convenience and same-site financing with manufacturer promotions for new vehicles, which can be appealing when you want to buy a car quickly. Credit unions tend to provide lower loan rates and more flexible terms, especially for members with strong credit histories. It's wise to compare offers from both to find the best loan.

Real-world insight: A dealer might present a buy-here-pay-here option or promotional APR for a new car, while a credit union will likely emphasize lower loan rates and customer service. Online auto lenders also offer competitive financing options and quick approvals that can beat dealership offers.

Can I negotiate financing at the car dealership?

Yes. Treat financing as a negotiable part of the car purchase. If you have a pre-approved loan, use it as leverage to get a better dealer financing offer or to negotiate a lower vehicle price. Dealers may counter with incentives such as cash back or a lower APR for qualified buyers.

Negotiation tips: Keep price negotiation separate from financing discussions, know the loan options you’ve been offered, and ask for the APR, fees, and loan term in writing. Compare the total interest and monthly car payment to determine which offer is best.

What happens to the loan balance if I want to pay off the loan early or refinance?

You can usually repay the loan early, which reduces the loan balance and saves on total interest. Some loans include prepayment penalties, so check loan documents before making extra payments. Refinancing can be a powerful option to lower your loan rate or reduce your monthly payment by choosing a new loan with better terms.

Example: If interest rates drop or your credit score improves after you get a car loan, refinancing to a lower APR could lower monthly car payments or shorten the loan term while keeping payments similar. Use an auto loan calculator to compare the savings in interest vs. any fees for refinancing.

When should I refinance my car loan?

Consider refinancing when you can secure a lower APR, have improved credit, or want to change the loan term to affect monthly payments. Ensure the savings in interest exceed any refinancing fees, and factor in the life of the loan to confirm you’ll benefit overall.

Checklist: Compare current loan rate, new loan rate, remaining loan balance, length of the new loan, and any costs or penalties to determine if refinancing is the best option.

How do I decide between leasing a car and purchasing the car with a loan?

Leasing a car typically offers lower monthly payments and the ability to drive a new car every few years, but you won’t own the vehicle and must adhere to mileage limits and return the car at lease end. Financing to purchase a car means you build equity and can pay off the loan to own the vehicle or trade it in later.

Consider this: If you want lower monthly car payments and frequent new vehicle upgrades, leasing might fit. If you prefer ownership and long-term cost savings, get a car loan and aim to pay off the loan, then keep the vehicle without monthly payments.

What are the long-term costs to compare when choosing lease vs. loan?

Compare total payments over the time you’ll keep the car, including down payment, monthly payment, insurance, maintenance, and potential fees for excess mileage or wear in a lease. Financing a car may have higher monthly payments initially, but once the loan is paid off you reduce transportation costs dramatically.

Tip: Use an amortization schedule or loan calculator to see how much interest you’ll pay over different loan terms and weigh that against lease costs and restrictions.

How can I make the auto financing process smoother and find the best loan?

Start by checking your credit report, saving for a down payment, and getting pre-approved. Use loan calculators to estimate monthly payment scenarios and compare loan offers from credit unions, banks, online lenders, and dealerships. A focused approach lets you choose financing options that align with your budget and buying goals.

Practical steps: Get multiple loan applications in a short window to limit credit score impact, review APR and loan term combinations, and insist on written loan offers. When buying a used car, verify the vehicle’s value and consider the car’s condition to avoid high maintenance costs that offset loan savings.

What red flags should I watch for in loan offers?

Beware of unusually high interest rates, hidden fees, long loan terms that dramatically increase total interest, and pushy dealers who mix monthly payment negotiation with price. Read disclosures carefully to understand the APR, loan principal, finance charges, and any prepayment penalties.

Red flag list: Very low monthly payments paired with a long loan term, balloon payments, mandatory add-ons that inflate the loan amount, and inconsistent APR disclosures. If unsure, consult a credit union or a trusted financial advisor before signing.

What practical examples show how easy auto financing process works from start to finish?

Example 1: Pre-approval to purchase the car. Sarah checks her credit report, gets pre-approved for a $15,000 loan at 4.5% APR for 48 months from her credit union, then shops for a used car within her budget. At the dealership she finds a reliable used car, negotiates the price, applies her $2,000 down payment, and completes the loan paperwork. Her monthly payment formula is set by loan amount, APR, and loan term using an auto loan calculator.

Example 2: Refinancing for better terms. John bought a new vehicle with a longer loan term to lower monthly payments but later improved his credit score. He refinances to a shorter loan term with a lower loan rate, lowers his life of the loan interest, and increases the principal pay-down each month to pay off the loan sooner.

How can using a loan calculator help me choose the best loan?

An auto loan calculator helps you input different loan amounts, APRs, and loan terms to see the monthly car payment and total interest. It lets you compare scenarios—shorter loan vs. longer loan, higher down payment vs. lower down payment—so you can choose a loan that meets your financial goals.

Use case: Plug in two loan offers to view principal and interest differences, determine how extra payments reduce the loan balance, and see the interest you'll pay over the life of the loan. This clarity helps you find the best loan for your situation.

How will understanding this process help me buy a car with confidence?

- Your credit score drives loan rate and approval

- Review credit report and correct errors before applying

- Compare APR, loan term, and total interest using an auto loan calculator

- Pre-approval or fact approval car loan gives negotiating power

- Larger down payments can secure lower interest and better terms

- Credit unions often offer competitive rates; dealerships provide convenience and incentives

- Refinancing can reduce interest or monthly payments if rates drop or credit improves

For buyers in Winter Garden, FL, local dealers like G7 Motor Sales can assist with used car financing and provide practical help to secure a fact approval car loan. Whether shopping for used cars in Winter Garden, FL, or considering a new car, understanding how to finance a car, compare loan options, and manage the monthly car payment will put you in the driver's seat.